TL;DR: Financial anxiety in high achievers often isn’t about the numbers; it’s about a nervous system still running on childhood programming. Early money messages and experiences get encoded as survival beliefs that logic and budgeting can’t fix. Approaches like EMDR that reprocess those root memories are what actually create lasting change.

Financial anxiety and childhood money beliefs aren’t always about the numbers.

Not because the numbers don’t work.

But because your nervous system hasn’t updated yet.

For many high-achieving professionals, financial anxiety isn’t about having too little. It’s about having enough, and still feeling like it could disappear at any moment.

What Financial Anxiety Actually Feels Like

Financial anxiety and childhood experiences are more connected than most people realize, and financial anxiety isn’t always about having too little money.

For many high-achieving professionals, it’s about having enough, or even more than enough, and still feeling chronically unsafe around finances.

This pattern shows up in distinct ways:

- You earn a solid salary but experience physical anxiety before every purchase, no matter how small.

- You’ve built substantial savings but never feel like it’s enough.

- You can negotiate brilliantly for clients or colleagues but freeze when it’s time to ask for your own raise.

- You check your bank balance compulsively, or avoid looking at it entirely, despite being financially responsible.

The disconnect is striking: objectively, your finances are stable. Subjectively, you feel one crisis away from collapse.

If you’re just beginning to explore this topic, the guide to what financial anxiety actually is unpacks how it differs from normal money stress and why it’s so common in high achievers.

Who This Affects

This pattern is particularly common among:

- High achievers who grew up with financial instability or scarcity messages

- Professionals who’ve climbed out of poverty or working-class backgrounds

- People who experienced sudden financial loss in childhood (job loss, divorce, bankruptcy)

- Those raised with confusing or contradictory messages about money and worth

- Individuals who experienced financial control or abuse in relationships

- First-generation professionals navigating class mobility

Why Traditional Financial Advice Doesn’t Resolve It

If you’ve tried budgeting apps, read money mindset books, worked with financial planners, or used logic-based reframing, and the anxiety persists, you’ve discovered an important truth. This isn’t a financial literacy problem. It’s a nervous system problem.

Your rational brain can look at your accounts and think “I’m financially secure.” But your survival brain is still operating on old programming that says “money equals danger” or “security is an illusion.”

Quick Self-Assessment

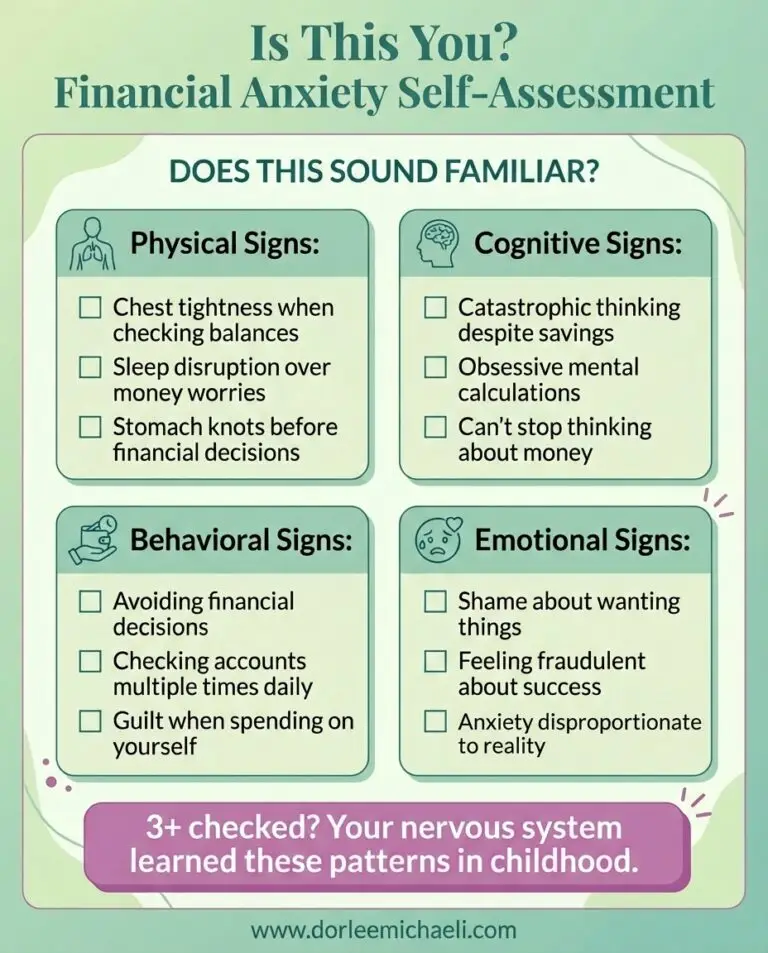

Financial anxiety rooted in childhood patterns often includes:

- Physical symptoms when thinking about money (chest tightness, shallow breathing, stomach tension)

- Guilt or shame about spending on yourself, even when you can afford it

- Difficulty articulating what you actually want financially because wanting feels dangerous

- Undercharging for your expertise or avoiding salary negotiations

- Feeling like financial success is fraudulent or undeserved (“I just got lucky”)

- Compulsive saving that never creates a felt sense of security

- Overworking to “prove” you deserve what you earn

THE NERVOUS SYSTEM EXPLANATION: WHY FINANCIAL ANXIETY AND CHILDHOOD PATTERNS PERSIST

Understanding why financial anxiety persists despite objective security requires understanding how your brain processes and stores emotional experiences, particularly experiences from childhood.

How Childhood Experiences Encode as “Truth”

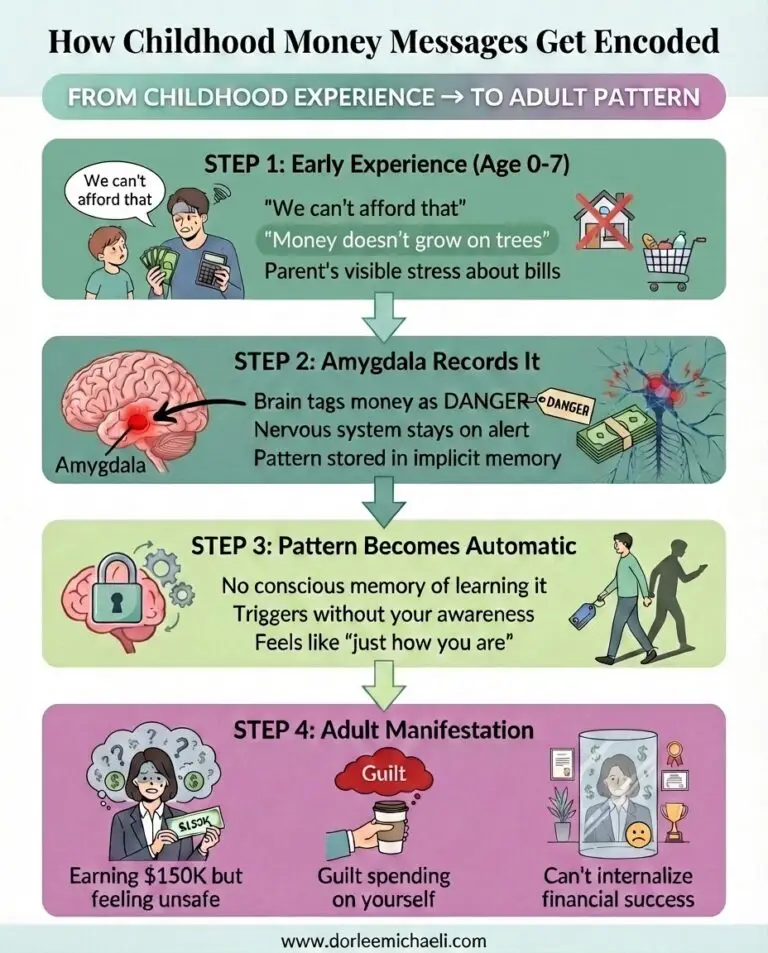

During childhood, your brain is highly receptive to learning about safety, danger, worth, and belonging. Experiences during this period get encoded in your nervous system not as memories you consciously recall, but as implicit beliefs about how the world works.

When you repeatedly witnessed financial stress in your household, or heard messages like “money doesn’t grow on trees” or “we can’t afford that,” your developing brain didn’t just note this information, a pattern of financial anxiety. It integrated it as fundamental truth about resources, safety, and your own worth.

These weren’t just words. They were emotional experiences that got stored in your body and nervous system as procedural memory, the kind of learning that operates automatically, below conscious awareness.

The Amygdala vs. Prefrontal Cortex Disconnect

Your brain has two key systems for processing information about money:

The Prefrontal Cortex (Rational Brain): This is the part that can look at your bank statement, see a healthy balance, and logically conclude “I’m financially secure.” It can create budgets, understand compound interest, and make rational financial plans.

The Amygdala (Threat Detection System): This is the part that stores emotional memories and scans for danger. If your childhood experiences taught your amygdala that “money = danger” or “spending = irresponsibility” or “security never lasts,” it will continue flagging financial situations as threats, regardless of what your rational brain knows.

The amygdala operates faster than conscious thought, a pattern of financial anxiety. It can trigger a full stress response (elevated heart rate, chest tightness, anxiety) before your prefrontal cortex even registers what’s happening. This is why you can know intellectually that you’re financially stable while your body insists otherwise.

Why Logic-Based Approaches Fail

When you try to fix financial anxiety with budgeting, affirmations, or logic-based reframing, you’re asking your prefrontal cortex to override your amygdala. But the amygdala doesn’t respond to logic; it responds to safety signals.

This is like trying to convince yourself not to flinch when something flies at your face. The flinch happens before thought. The same is true for financial anxiety and childhood-encoded patterns: the threat response activates before rational analysis can intervene.

To create lasting change, you need to update the programming in your survival brain, not just override it with willpower.

The Role of Threat Detection in Financial Decision-Making

When your nervous system perceives money as a threat, it influences every financial decision you make:

- You avoid making investment decisions because choosing feels dangerous

- You undercharge for your work to avoid the vulnerability of being told “no”

- You save compulsively because spending triggers your threat response

- You delay career moves that would increase income because success feels fraudulent

- You work constantly to “prove” your worth because rest triggers anxiety about deserving what you earn

These aren’t character flaws. They’re protective responses from a nervous system that learned early that money was tied to safety, worth, and survival.

The Childhood Origins of Financial Anxiety and Money Beliefs

Financial anxiety doesn’t emerge from nowhere. It has identifiable origins in your lived experience: what you saw, heard, and learned about money during your developmental years.

Childhood Money Messages and Their Long-Term Impact

The messages you received about money in childhood weren’t neutral information, a pattern of financial anxiety. They were emotional lessons about worth, safety, and belonging that created lasting neural pathways.

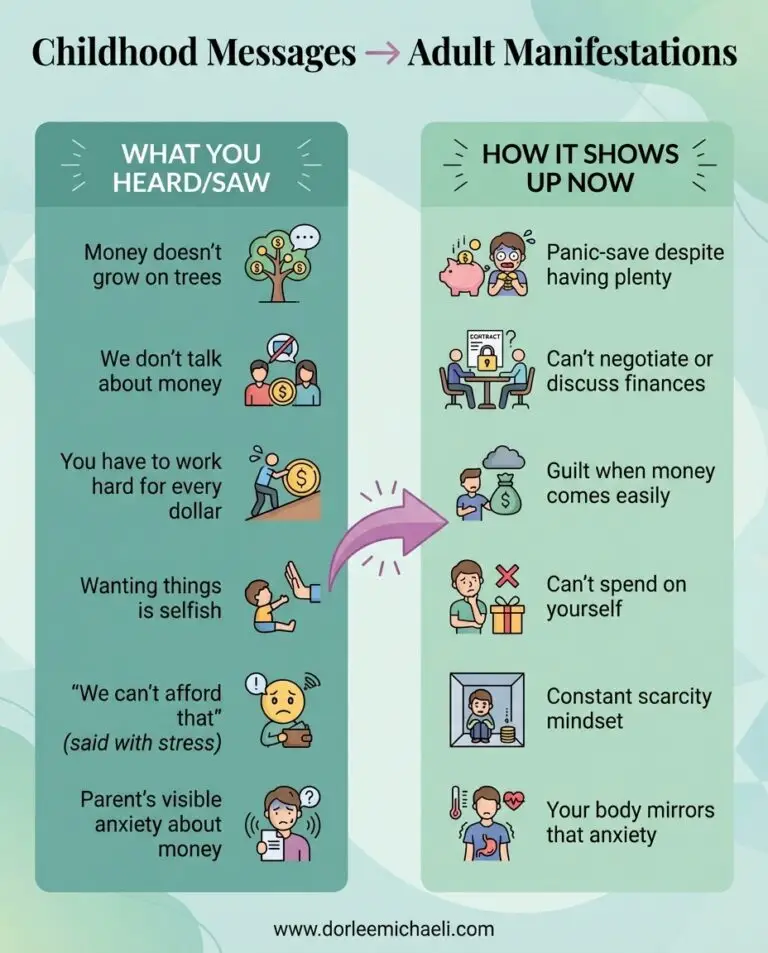

Common childhood messages and their adult manifestations:

“Money doesn’t grow on trees”

→ Adult belief: Resources are fundamentally scarce; spending is dangerous

→ Behavior: Panic-checking bank balance before small purchases, difficulty spending on yourself even when financially stable

“We don’t talk about money”

→ Adult belief: Money is shameful, taboo, or dangerous to discuss

→ Behavior: Inability to negotiate salary, discomfort discussing finances with partners, avoiding financial planning

“You have to work hard for every dollar”

→ Adult belief: Ease equals unworthiness; suffering proves value

→ Behavior: Sabotaging opportunities that feel “too easy,” guilt when money comes without struggle, overworking to justify income

“Wanting things is selfish”

→ Adult belief: Having needs or desires makes you bad

→ Behavior: Inability to spend on yourself without shame spirals, difficulty articulating financial goals, chronic self-deprivation

“We can’t afford that” (said with stress or shame)

→ Adult belief: Your worth is measured by what you can provide; scarcity is your fault

→ Behavior: Overworking to prove worthiness, feeling responsible for others’ financial wellbeing, guilt about having more than family of origin

What You Saw: Modeling and Implicit Learning

Beyond explicit messages, children absorb lessons about money through observation:

- Watching parents fight about money taught you that finances create conflict and threaten relationships

- Witnessing a parent’s anxiety about bills taught you that money equals danger

- Seeing money used as control taught you that financial dependence is unsafe

- Observing secrecy around finances taught you that money is shameful

- Experiencing your family’s stress during economic hardship taught you that security is always temporary

These patterns get internalized as “how money works” and “what money means,” often without conscious awareness.

Financial Instability and Sudden Change

Experiencing financial instability during childhood, especially sudden or dramatic changes, can create lasting hyper-vigilance around money:

- A parent losing their job and the household shifting from comfortable to struggling

- Divorce leading to sudden financial insecurity

- Bankruptcy, foreclosure, or eviction

- Moving from financial stability to poverty (or vice versa)

- Watching a parent’s business fail

- Economic recession affecting your family directly

These experiences teach your nervous system that financial security can disappear without warning, creating chronic anxiety even when your current situation is objectively stable.

Intergenerational Patterns

Money beliefs often pass through generations:

- Your grandparents who survived the Great Depression taught your parents that scarcity is always lurking

- Your parents’ financial trauma (poverty, debt, loss) became your inherited anxiety

- Cultural or religious messages about money and worthiness shaped your family’s relationship with finances

- Immigration experiences of financial precarity created lasting beliefs about safety and risk

You may be the first generation to achieve financial stability, but still carrying the nervous system programming of scarcity from previous generations.

Systemic Factors

Financial anxiety isn’t just personal; it’s shaped by larger systems:

- Class background and mobility: Moving between socioeconomic classes creates unique psychological tensions

- Racial and ethnic factors: Systemic barriers to wealth accumulation create different relationships with money and security

- Gender socialization: Different messages about money, worth, and deserving based on gender

- Economic instability: Growing up during recessions, housing crises, or periods of high unemployment

When “Enough” Was Never Defined

Many people with financial anxiety never received a clear definition of “enough” in childhood:

- There was no model for what financial security looks like

- Success was always defined by “more” with no endpoint

- Survival mode meant there was never space to define adequacy

- Worth was tied to achievement with constantly moving goalposts

Without an internal sense of “enough,” no amount of money ever feels secure.

How Financial Anxiety Shows Up in Daily Life

Financial anxiety and childhood roots manifest across cognitive, emotional, behavioral, physical, and relational domains, often in ways that feel confusing precisely because they’re disproportionate to your current reality.

Cognitive Patterns

- Avoidance: Not opening bills, avoiding checking account balances, postponing financial decisions, ignoring investment accounts despite being financially responsible in other ways.

- Obsessive tracking: Checking accounts multiple times daily, tracking every penny, creating elaborate spreadsheets, needing constant confirmation of financial status.

- Catastrophizing: Assuming worst-case scenarios (“I’ll end up homeless”), believing current stability is temporary, waiting for inevitable financial disaster.

- Minimizing success: Attributing financial achievements to luck rather than competence, dismissing accomplishments, believing you’ve fooled people.

Emotional Responses

- Shame: Feeling bad about spending on yourself, guilt about having more than family of origin, embarrassment about financial topics.

- Guilt: Believing you don’t deserve financial security, feeling wrong for wanting things, experiencing distress when spending even reasonable amounts on yourself.

- Anxiety: Persistent worry about money despite stability, panic about future scenarios, generalized financial dread.

- Dissociation: Feeling disconnected from financial reality, numbness around money topics, spacing out during financial discussions.

Behavioral Manifestations

- Undercharging: Setting rates below market value, lowering prices immediately when questioned, avoiding negotiations, working for less than you’re worth.

- Compulsive saving: Saving far beyond what’s needed for security, inability to spend savings even for intended purposes, hoarding without clear goals.

- Self-sabotage: Missing opportunities for advancement, avoiding raises or promotions, turning down higher-paying work, undermining own success.

- Overworking: Working excessive hours to prove worthiness, taking on too much, inability to rest without guilt, productivity as proof of value.

- Overspending: For some, anxiety manifests as compulsive spending, retail therapy, or using purchases to regulate emotions.

Physical Symptoms

Financial anxiety often creates somatic responses:

- Chest tightness or pressure when thinking about money

- Shallow breathing during financial discussions

- Stomach tension or nausea around purchases

- Elevated heart rate when checking accounts

- Muscle tension, headaches, or fatigue related to financial stress

- Sleep disruption from money worries

Relational Impacts

Financial anxiety affects relationships:

Conflict: Fighting with partners about spending, difficulty making joint financial decisions, defensiveness about money topics.

Secrecy: Hiding purchases, maintaining separate accounts from partners, inability to be transparent about finances.

Control dynamics: Using money to control others, being controlled by others through finances, power imbalances.

Isolation: Avoiding social situations that require spending, declining opportunities due to financial anxiety, withdrawing from friends.

Understanding Financial Anxiety vs. Related Patterns

Understanding the distinctions between related patterns helps clarify what you’re experiencing and what kind of support might help.

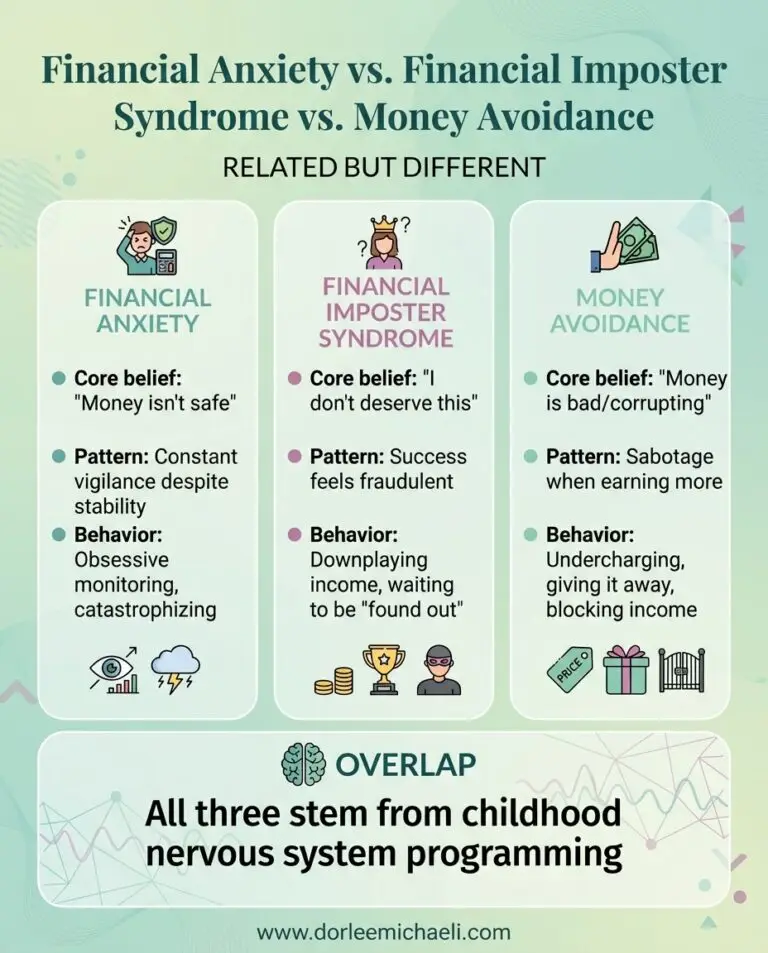

Financial Imposter Syndrome

Financial imposter syndrome is the subjective experience of feeling like your financial stability isn’t real or deserved, despite objective evidence otherwise.

Key features:

- Attributing financial success to luck, timing, or others’ help rather than your own competence

- Feeling like a fraud about your income or savings

- Believing you’ve somehow fooled people into thinking you’re financially competent

- Fear of being “found out” as not deserving your financial position

- Dismissing or minimizing your financial achievements

Financial imposter syndrome often coexists with workplace imposter syndrome, both stemming from the same root belief that your worth is conditional and must be constantly proven.

Money Avoidance vs. Money Vigilance

Research in financial psychology identifies different “money scripts,” unconscious beliefs about money that drive behavior.

Money Avoidance: Believing money is bad, that having wealth makes you greedy or corrupt, that you don’t deserve money. This manifests as avoiding financial decisions, self-sabotaging opportunities, or giving money away compulsively.

Money Vigilance: Believing you must be alert and watchful about finances, that financial disaster is always possible. This manifests as secretiveness about finances, anxiety about spending, or difficulty enjoying money.

Many people experience both patterns simultaneously, avoiding financial decisions while remaining hyper-vigilant about security.

When Anxiety Becomes Disordered

While not a formal diagnosis, financial anxiety can become severe enough to significantly impair functioning:

- Panic attacks triggered by financial topics or decisions

- Complete avoidance of necessary financial tasks (paying bills, filing taxes, opening mail)

- Obsessive-compulsive patterns around money (checking accounts hundreds of times daily)

- Depression or hopelessness related to finances despite objective stability

- Relationship breakdown due to money-related conflicts

- Career impairment from inability to negotiate or accept opportunities

Normal Financial Stress vs. Nervous System Dysregulation

The key distinction:

Normal financial stress: Worry that’s proportionate to your actual situation. If you’re struggling to pay bills, stress makes sense. If you’re facing job loss or major expenses, anxiety is situational and appropriate.

Nervous system dysregulation: Anxiety that’s disproportionate to your actual financial situation. You have savings, steady income, no immediate crisis, yet you experience chronic financial fear, physical symptoms, and persistent sense of insecurity.

When to Seek Professional Help

Consider professional support if:

- Financial anxiety persists despite objective stability

- You experience physical symptoms (panic, chest pain, insomnia) related to money

- Traditional financial advice hasn’t resolved the anxiety

- You avoid necessary financial decisions despite having resources

- Money anxiety is affecting relationships, career, or quality of life

- You recognize childhood patterns but can’t shift them alone

- You want to understand what’s really driving your financial behaviors

What Actually Heals Financial Anxiety: Treatment Approaches

Healing financial anxiety requires addressing the nervous system patterns that maintain it, not just managing symptoms or forcing behavioral change.

Why Nervous System Reprocessing Is Different from Mindset Work

Traditional mindset approaches say: “Think differently about money. Use affirmations. Reframe your beliefs.”

The problem: You’re asking your rational brain to override your survival brain. That’s like trying to convince your body not to flinch when something flies at your face. The flinch happens before thought.

Nervous system approaches work differently: Instead of trying to override threat responses with willpower, they help your brain reprocess the experiences that created those responses in the first place.

EMDR therapy for Money Belief Updating

Eye Movement Desensitization and Reprocessing (EMDR) is an evidence-based therapy originally developed for trauma that’s highly effective for updating money beliefs rooted in childhood.

How EMDR therapy works for financial anxiety:

- Identifying target memories: Working with a therapist, you identify specific moments where money became linked with worth, safety, or survival, like witnessing parental fights about money, being shamed for wanting something, or experiencing financial instability.

- Exploring associated beliefs: What did those moments teach you? “I’m only valuable if I’m productive,” “Money will always run out,” “Wanting things makes me selfish.”

- Bilateral stimulation: While recalling the memory, you engage in bilateral stimulation (eye movements, tapping, or audio tones). This activates both brain hemispheres and facilitates reprocessing.

- Natural processing: Your brain digests the experience. The emotional charge fades. New insights emerge. The memory remains, but it no longer triggers your threat response.

- Integration of new beliefs: Not through forced affirmations, but through genuine nervous system shifts: “My worth isn’t conditional,” “I can build security,” “Having needs is human.”

What changes after EMDR:

- You check bank balances without chest tightening

- Spending on yourself doesn’t trigger guilt

- Financial discussions feel manageable

- You negotiate for raises without freezing

- Success feels real, not fraudulent

- Money becomes a tool, not a measure of worth

To learn more about how this process works in practice, visit the page on EMDR therapy for imposter syndrome and financial anxiety.

Somatic Therapy and Nervous System Regulation

Somatic approaches address how financial anxiety lives in your body:

- Tracking physical sensations that signal threat responses

- Learning to regulate nervous system activation

- Building capacity to tolerate discomfort around money

- Creating new somatic associations with financial security

These approaches help you notice when your body shifts into threat mode around money, and develop skills to return to a regulated state.

Financial Social Work Integration

Financial social work is a specialized practice that addresses the emotional, psychological, and systemic dimensions of money, not just the technical ones. Unlike traditional financial planning, which focuses on what you should do with money, financial social work explores why you can’t do what you already know you should.

It recognizes that financial behaviors are shaped by childhood experiences, cultural messages, relational patterns, and nervous system programming, and that lasting change requires addressing those roots directly. Working with a financial social worker means you’re not just building a budget; you’re rebuilding your relationship with money from the inside out.

This approach addresses both the psychological roots of financial anxiety AND the practical financial planning needed to build security.

What to Expect in Treatment

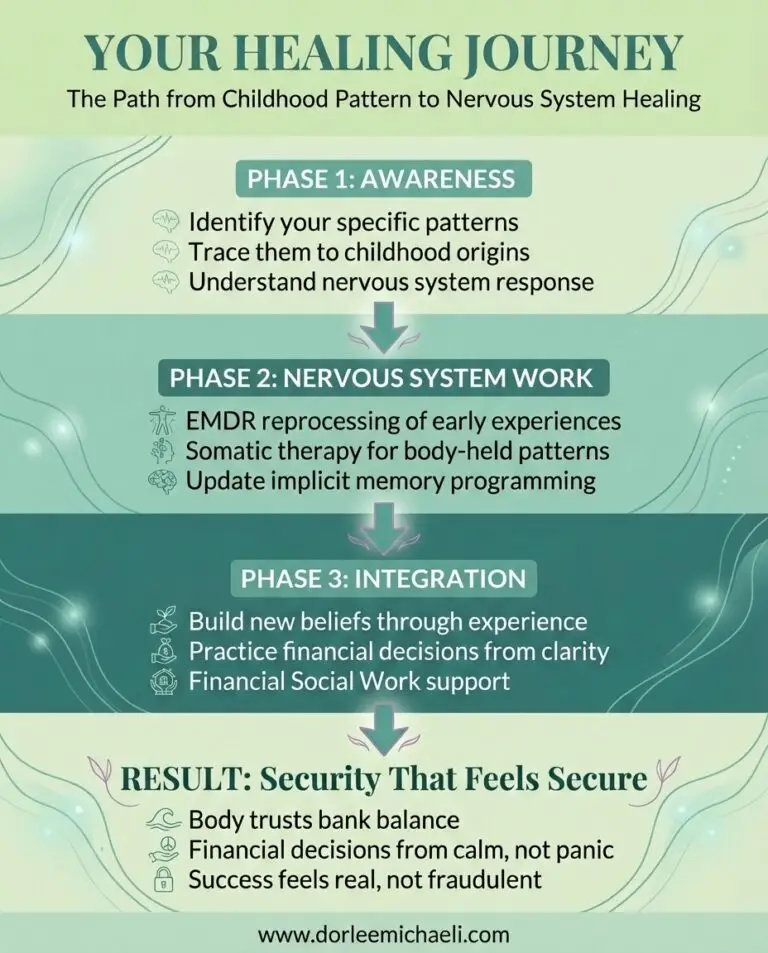

Healing your relationship with money typically involves:

Phase 1: Understanding your money story

Exploring childhood experiences, identifying current patterns, understanding how beliefs formed

Phase 2: Reprocessing target memories

Using EMDR or other approaches to update nervous system programming

Phase 3: Building new patterns

Practicing financial decisions from a regulated state, creating meaningful plans, integrating new beliefs

Phase 4: Consolidation

Strengthening changes, addressing remaining patterns, developing sustainable relationship with money

Change happens naturally as your nervous system updates—not through forcing yourself to behave differently.

Finding the Right Support

What to Look For in a Therapist

When seeking help for financial anxiety and childhood-rooted patterns, look for:

- Training in trauma-informed approaches (EMDR, somatic therapy, IFS)

- Understanding of money psychology and financial behaviors

- Recognition that this is a nervous system issue, not a budgeting problem

- Ability to address both psychological patterns AND practical financial planning

- Comfort working with high-achieving professionals

Specialized Credentials

Financial Social Work: Training in both clinical social work AND financial psychology. Financial Social Workers understand systemic factors, money psychology, and therapeutic approaches.

EMDR Certification: Training in Eye Movement Desensitization and Reprocessing for trauma and emotional memory reprocessing.

Financial Therapy: Integration of therapeutic and financial planning skills, though approaches vary.

Questions to Ask

When consulting with potential therapists:

- “How do you work with financial anxiety that’s rooted in childhood experiences?”

- “Do you use approaches that address nervous system patterns, not just behavior change?”

- “What’s your understanding of the connection between money beliefs and worthiness?”

- “Can you help with both the psychological patterns and practical financial planning?”

- “What does the typical treatment process look like?”

When to Combine Therapy with Financial Planning

Some situations benefit from working with both a therapist AND a financial planner:

- Complex financial situations requiring specialized planning expertise

- Major financial decisions (buying property, starting business, retirement planning)

- When you need both nervous system healing AND technical financial guidance

The therapist addresses the psychological patterns; the planner provides technical expertise. Ideally, they communicate to create coordinated support.

Moving Forward: Security That Feels Secure

Financial anxiety and childhood programming aren’t about poor money management.

They’re about a nervous system that learned early that money equals danger, that worth is conditional, that security is always temporary.

Healing doesn’t mean you’ll suddenly spend recklessly or stop caring about financial responsibility.

It means:

- Financial stability will finally feel stable

- Success will feel real and earned, not fraudulent

- You’ll make decisions from clarity instead of fear

- Spending on yourself won’t trigger shame spirals

- Your worth won’t depend on constant productivity

- You’ll build toward a vision that actually matters to you

Financial security isn’t just about the numbers in your account. It’s about the internal sense that you’re safe, that you’re enough, that your worth isn’t conditional on constant proof.

That internal shift is possible. Your nervous system can learn new patterns. The beliefs installed in childhood can be updated.

Not through willpower. Not through better budgeting. But through approaches that work with how your brain actually stores and processes emotional memories.

You don’t need to be in financial crisis to deserve support. You just need to be ready to understand your relationship with money and change the patterns that no longer serve you.

References

Bravata, D. M., Watts, S. A., Keefer, A. L., Madhusudhan, D. K., Taylor, K. T., Clark, D. M., … & Hagg, H. K. (2020). Prevalence, predictors, and treatment of imposter syndrome: A systematic review. Journal of General Internal Medicine, 35(4), 1252–1275.

Chen, Y. R., Hung, K. W., Tsai, J. C., Chu, H., Chung, M. H., Chen, S. R., … & Chou, K. R. (2014). Efficacy of eye-movement desensitization and reprocessing for patients with posttraumatic-stress disorder: A meta-analysis of randomized controlled trials. PLoS ONE, 9(8), e103676.

Clance, P. R., & Imes, S. A. (1978). The imposter phenomenon in high achieving women: Dynamics and therapeutic intervention. Psychotherapy: Theory, Research & Practice, 15(3), 241–247.

de Jongh, A., Resick, P. A., Zoellner, L. A., van Minnen, A., Lee, C. W., Monson, C. M., … & Bicanic, I. A. (2024). State of the science: Eye movement desensitization and reprocessing (EMDR) therapy. Journal of Traumatic Stress, 37(1), 7–23.

KeyBank. (2025). Financial imposter syndrome: Navigating perception vs. reality in 2025. KeyBank 2025 Financial Mobility Survey.

Klontz, B., Britt, S. L., Mentzer, J., & Klontz, T. (2011). Money beliefs and financial behaviors: Development of the Klontz Money Script Inventory. Journal of Financial Therapy, 2(1), 1–22.

Shapiro, F. (2018). Eye movement desensitization and reprocessing (EMDR) therapy: Basic principles, protocols, and procedures (3rd ed.). Guilford Press.

Smith, C. E., Hao, J., Olson, J., Ghosh, R., & Rick, S. (2024). Spendthrifts and tightwads in childhood: Feelings about spending predict children’s financial decision making. Journal of Behavioral Decision Making, 37(1), e2333.

Wolfsohn, R., & Schwartz, M. L. (2024). Financial social work: Micro, mezzo, and macro practice. Cognella Academic Publishing.